Senator Bernie Sanders (I-VT) and Representative John Larson (D-CT) recently introduced legislation to ensure that the Social Security Administration (SSA) has the resources it needs to provide beneficiaries with the services and support they deserve. The Social Security Administration Fairness Act (S.3147/H.R. 6251) establishes a set funding level for SSA equal to a percentage of the overall benefit payments the agency pays out. The legislation would also impose a moratorium on Social Security field office closures to halt the loss of additional field offices.

In addition, the legislation would also assist those eligible for or receiving disability benefits. Currently, those approved for Social Security Disability Insurance benefits are subject to a five-month waiting period before they can receive disability benefits and must wait two years before they are eligible for Medicare. This delay in disability or health care benefits can be detrimental for people already dealing with the effects of a serious disability, in addition to other health problems. Sanders’s legislation would eliminate these waiting periods for disability recipients, allowing them to immediately access disability benefits and Medicare coverage.

Co-sponsors to this legislation in the Senate are Senators Elizabeth Warren (D-MA), Kirsten Gillibrand (D-NY), Jeff Merkley (D-OR), Cory Booker (D-NJ), Sheldon Whitehouse (D-RI), and Brian Schatz (D-HI). The corresponding legislation in the House of Representatives has over 30 co-sponsors.

We’ll be tracking and reporting on any progress on the bill. Advocates can show their support for the bill by writing or calling their Member of Congress and asking them to sign on in support or thanking them for co-sponsoring.

Since 1956, the Social Security program has provided cash benefits to people with disabilities. This annual report provides program and demographic information about the people who receive those benefits. The basic topics covered are—

beneficiaries in current-payment status;

workers’ compensation and public disability benefits;

benefits awarded, withheld, and terminated;

disabled workers who have returned to work;

outcomes of applications for disability benefits; and

disabled beneficiaries receiving Social Security, Supplemental Security Income, or both.

Profile of Disabled-Worker Beneficiaries

Workers accounted for the largest share of disabled beneficiaries (87 percent).

Average age was 54.

Men represented less than 52 percent.

The largest category of diagnoses was diseases of the musculoskeletal system and connective tissue (32.3 percent).

Average monthly benefit received was $1,171.15.

Supplemental Security Income payments were another source of income for about one out of eight.

Awards to disabled workers (706,448) accounted for 88 percent of awards to all disabled beneficiaries (799,330).

Benefits were terminated for 820,372 disabled workers.

A thought-provoking article about the Social Security Disability (SSD) program appeared in the August 25, 2014 edition of The Hill, a newspaper published for and about the U.S. Congress. The article was authored by Barbara Silverstone, Executive Director of NOSSCR, the National Organization of Social Security Claimant’s Representatives. Ms. Silverstone’s complete article can be accessed on the The Hill’s website.

Ms. Silverstone dispels with factual data some of the myths currently being peddled by certain members of Congress and media outlets. Ms. Silverstone points out the eligibility criteria for SSD are extremely strict, and the burden is on the person applying for benefits to prove, with medical records – not mere assertions, the severity of his or her disabling condition(s). Only about 40% of applications are approved, a fact that belies the claim there is a systematic bias toward approving applicants who are not actually disabled. The current approval rate is the lowest it has been in 40 years.

Ms. Silverstone notes that recent Congressional investigations into allegations of fraud have not identified any cases of fraud beyond those that the Social Security Administration itself has uncovered. She discusses, in particular, the 2012 investigation of Senator Coburn. His staff reviewed about 300 appeals decisions, but failed to identify a single individual who was approved for benefits that should have been denied. Congress complains that the Social Security Administration does not do enough to identify potential fraud in the program, but at the same time Congress has cut Social Security’s budget, providing about $1 billion less than requested over the past three years! As a result, Social Security has lost more than 11,000 employees since 2011. This inevitably has impacted the agency’s ability to serve the American people in many aspects of its operation.

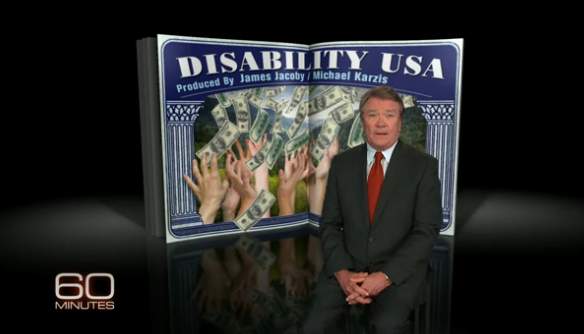

Just in time for a scheduled meeting of the Senate Committee on Governmental Affairs to discuss the status of the Social Security Disability program (SSDI) on October 7th, on Sunday, October 6, CBS’ popular “news” show, 60 Minutes, aired “Disability USA” – a sensationalized program full of misleading and largely anecdotal information designed to convince viewers the program is riddled with fraud and on the brink of collapse. If you watched this program, and it is your sole source of information about Social Security Disability, you know essentially nothing about the actual operation of the program. You heard not a single word from disability recipients, their advocates, or from officials who administer the program, none of whom were invited to participate in the 60 Minutes piece.

…the 60 Minutes segment focused on some fraud in the program in one impoverished area of the country in order to paint disability recipients generally as the undeserving poor, slackers and frauds.

First, listening to the program you might not have understood that the average monthly benefit of about $1100 is not tax-payer money but earned credits for money paid into the system by the disabled worker. Then, in terms of the “shocking” growth of the disability rolls you heard CBS’s Steve Kroft and Senator Tom Coburn, R-Oklahoma natter on about, you didn’t hear that the statistical growth of the program is a direct function of the increase in population over the past 30 years, the aging of the baby-boomer population into their higher disability years, the entry of women into the work force in greater numbers, and similar demographic factors. Finally, you likely came away from the program thinking that qualifying for SSDI is a cakewalk, when the actual standards for disability result in denial of two-thirds of all applications, only 10% of those denials being reversed on appeal, and an overall figure of about 41% of applicants ultimately qualifying.

Completely ignored in this puff-piece for the right wing (Coburn is the lead Republican on the Senate Subcommittee for Investigations and has a long-standing, well-documented hostility to Social Security) is the shifting of responsibility for disability from workers’ compensation systems, where it properly belongs, to the Social Security Disability program because of the rollbacks in coverage and benefits in states’ workers’ comp programs across the country, all driven by right-wing and corporate interests. So, while SSDI faces potential exhaustion of its funds in the next few years (although this can be – and in the past has been – remedied by shifting funds from the Social Security old-age program), the liability insurance industry, which includes workers’ compensation carriers, is enjoying record profits over the last two years.

Similarly unmentioned was the impact of the worst economy in decades, shrinking the ability of disabled workers to find less physically challenging work.

As is typically the case with these types of “news” pieces, the 60 Minutes segment focused on some fraud in the program in one impoverished area of the country in order to paint disability recipients generally as the undeserving poor, slackers and frauds. CBS could have moderated the potential negative impact of its program by including interviews of SSA program officials or of spokespersons from some two dozen national disability advocacy organizations who asked to be heard on this show. It shamefully chose to ignore all such requests, and has diminished itself accordingly as a news organization.

Today’s post comes from guest author Susan C. Andrews, from Causey Law Firm.

You hear it all over the place these days: there are lots of people out there who lied and cheated to get Social Security Disability (SSD) benefits. I’m here to tell you that is a myth. You don’t have to drill down very far to find out differently. I should know, from where I sit, as an attorney who handles SSD cases. Where I sit most days is in front of a big pile of medical records—I mean HUNDREDS of pages of medical records, all belonging to the same person. You see, some of my clients have just one great big medical issue—like cancer, or Multiple Sclerosis, or Parkinson’s, and many of my clients have multiple medical problems. Either way, they have spent more time in doctors’ offices and hospitals than any of us would ever choose to do.

There is a mistaken notion floating around out there that a person can just waltz into Social Security, claim to be disabled, and voila—he’s granted benefits!

There is a mistaken notion floating around out there that a person can just waltz into Social Security, claim to be disabled, and voila—he’s granted benefits! Nothing could be further from the truth. The burden of proof is on the claimant (the person claiming benefits) to show that he or she is disabled from engaging in substantial gainful activity (SGA) for a period of at least 12 continuous months. More about SGA in a bit. That proof starts with medical records, and diagnoses made by doctors. Self-diagnosing just doesn’t cut it, even if you’ve read up on your condition all over the internet, and you’re absolutely positive you know what’s wrong with you! Sometimes we get calls from people who do not have health insurance, and even though they have a serious medical condition, they have been unable to access much in the way of health care. Sadly, some of those folks who should be able to qualify for benefits do not, because they simply do not have the necessary treatment records to document the seriousness of their conditions.

As mentioned above, Social Security’s definition of disability is the inability, due to one or more medical impairments, to engage in substantial gainful activity for a period of at least 12 continuous months. Social Security defines SGA in part by a dollar figure that usually goes up a little every year. In 2013 it is $1,040. Social Security looks at a person’s GROSS earnings, not net earnings or take-home pay. So if I’m able to gross $1,040 or more per month, I can engage in substantial gainful activity and I do not qualify for SSD. This concept is important especially for individuals with progressive conditions.

Take, for example, a person diagnosed with Parkinson’s. One famous example is the actor Michael J. Fox. His Parkinson’s affects his functioning, but he is still working. Many people with progressive conditions continue to work for some time after receiving their diagnosis. At some point, progression of the disease may force some of them to go to part-time work. When the hours worked decrease, their earnings may no longer qualify as SGA. Or—and I see this a great deal in my practice—some people begin to have more bad days than good days, and work performance is impacted. There are days so bad that they really have no choice but to call in sick. Then this begins to happen more frequently than a couple of days a month. In my experience, at that point most employers become very unhappy campers. Not only are the employees taking sick leave faster than they are accruing it, they can’t tell their employers ahead of time which days they will wake up with an exacerbation of symptoms that keep them in bed, or at least in their bathrobe, all day.

Which brings me to my final point: Many of my clients look okay to the casual passer-by. Take the guy with a serious heart problem. Well sure, if I followed him around for half a day, I’d see that he can barely exert himself without getting out of breath. But if I just passed by, he might look fine. And the day he spends at home in his bathrobe because he can hardly catch his breath—I’m not going to see him at all when he’s having one of those really lousy days. His condition may be largely invisible.

To sum it up, I’d say there’s a bit of wisdom in being slow to judge. Thank goodness we take our good health for granted—it’d be a miserable existence if I spent too much time worrying about getting sick before it actually happened. But, of course, serious illness can strike any of us when we least expect it. And on the other side of that defining moment, the world can look a whole lot different.

A person who has been out of the labor market for quite some time before he applies for Social Security Disability (SSD) may find that his application for benefits is rejected because he cannot prove he became disabled before his date last insured. In order to qualify for benefits in the first place, a person must pay Social Security taxes long enough to have insured status. When the individual stops working and therefore stops paying into the system, eventually he will hit his date last insured and lose his insured status. It is a little like a private insurance policy: when you stop paying the premiums, you no longer are covered by the policy. For a person who has work steadily in his lifetime, the date last insured is arrived at and insured status lapses about five years after stopping work.

The Social Security Administration has another program for the medically disabled called Supplemental Security Income (SSI) where there is no date last insured rule, but there are other program requirements and limitations. In a future article, we will explore the differences between the Social Security Disability (SSD) and Supplemental Security Income (SSI) programs.

As an example of how the date last insured issue can prevent a person from getting Social Security Disability (SSD) benefits, consider the case of a 35 year-old woman who has worked steadily since her late teens. She and her husband have twins when she is in her mid-30s. There are a lot of late night feedings and diapers to change! She stays home to take care of the twins while her husband continues to work to support the family. When the twins turn five, she begins to think about returning to work, perhaps when they go into first grade a year or so later. Five years has passed, and she reaches her date last insured. She loses her insured status and has not yet returned to work. When the twins turn six, she gears up her job search, but has not yet re-entered the labor market. Then medical catastrophe strikes: she has a very disabling stroke – unusual in a person this young, but not unheard of. She clearly cannot work. She applies for Social Security Disability and is turned down because she did not become disabled before her date last insured. Unlike the Social Security Retirement program, where it is possible to collect Social Security Retirement (SSR) benefits on the earnings record of one’s spouse, the Social Security Disability program only allows for benefits to be paid on the basis of one’s own earnings record.

Consider another scenario with this family of four. When the twins are three, mom is diagnosed with Multiple Sclerosis. This condition can progress slowly or more quickly. In her case, she suffers a fairly quick progression of symptoms. By the time the twins are six and going into first grade, she is ready to return to work, except that she is suffering a variety of MS symptoms, including the profound fatigue that is experienced by many with this disease. Her combination of symptoms prevents her from working, so she applies for Social Security Disability. She passed her date last insured when the twins turned five. Will she get benefits? That depends. She certainly can apply for benefits after her date last insured, but she must be able to show that her symptoms had become sufficiently severe to prevent her from working before her date last insured. We have handled many cases where the individual is out past his or her date last insured. The key is to obtain all of the medical records that help to document the seriousness of the medical condition before that date last insured. Sometimes these can be buttressed with statements from family members or close friends who were in a position to observe at close range how seriously the person’s medical condition was affecting her functioning prior to the date last insured. In the case above, a statement from the husband likely would be helpful.

The Social Security Administration has another program for the medically disabled called Supplemental Security Income (SSI) where there is no date last insured rule, but there are other program requirements and limitations. In a future article, we will explore the differences between the Social Security Disability (SSD) and Supplemental Security Income (SSI) programs.

Applications for Social Security Disability now can be filed online.

We get many calls from folks who have been off work for a while, and are wondering if the time is right to place an application for Social Security Disability benefits. There are several program rules that should be kept in mind in making this decision.

The first thing to know about Social Security Disability is that it is a program for people who have one or more health issues that prevent the person from working for a period of at least 12 continuous months. If you have not yet been off work for that length of time, but anticipate that may be the case, you may want to go ahead and apply, since the entire process can take months and, in some cases, a year or more, before a final decision is made. On the other hand, if you are fairly confident you will be able to get back to work before 12 months has passed, then holding off makes more sense.

…benefits can go back no more than one year from the date of the application. This is a matter of concern for those who hold off too long and, as a result, lose out on benefits to which they are entitled.

To collect any benefits at all, one must satisfy the above-described 12-month duration requirement. That said, once a person has satisfied the 12-month rule, it also is helpful to know that benefits cannot begin until five full months after the date of the onset of disability. So, for example, if I am diagnosed with a cancer and, because of my treatment, I must stop working on June 7, 2013, (and I know, because of the course of proposed treatment, that I am likely to be off work for more than 12 continuous months), then I could apply right away, but benefits would not begin until December of 2013. The five full months that I must wait for benefits to begin (in this example, July through November) is called the waiting period. The month of June cannot be counted because it is not a full month. Thus, if there is some possibility I might be able to return to work before 12 months has passed, depending on how my treatment goes, then I might want to hold off initially, to see how it goes.

The other rule to keep in mind is that benefits can go back no more than one year from the date of the application. This is a matter of concern for those who hold off too long and, as a result, lose out on benefits to which they are entitled. So in the example above, I stop working due to cancer treatment on June 7, 2013. That is my onset of disability date. I think I will be able to go back to work in less than 12 continuous months, so I do not apply. Complications ensue, and I am still off work one year later, past June 7 of 2014. Maybe at that point I am feeling really exhausted and unwell from all of the treatment and/or the cancer, so I just cannot get organized to apply for benefits. By the time I apply, it is March of 2015. Benefits can go back no further than March of 2014, even though I satisfied the five month waiting period in December of 2013. Assuming my case is approved for benefits, I lose out on benefits for that month and January and February of 2014 because I waited too long to apply. To avoid this consequence, one should apply no more than 17 months after stopping work due to the disabling health problem.

Applications for Social Security Disability now can be filed online. While this eliminates the need to go in person to a Social Security office to apply, the process, before all is said and done, still can be quite daunting. For this reason, we are available to assist you with the online application. The Social Security Administration has an informative website, where you can access the online application. If you are thinking about applying for benefits, it is worth taking a look. If you have questions, feel free to give us a call. Here is the link:

If you, or a loved one, are diagnosed with a severe or aggressive condition, you may qualify to be immediately approved!

One question that I am asked frequently by folks considering applying for Social Security Disability is “How long do I need to be off work?” This question is based on a slight misunderstanding of the Social Security rules. Your medical condition, or combination of conditions, that prevents you from working must have lasted or be expected to last a minimum of one year, (or be expected to result in death), in order for you to qualify for Social Security Disability. That year does not need to have passed, in order for you to file your application. If your condition is not expected to get better, or if a long course of treatment is planned that would take you out past one year, then you can file your initial application. If there is clear medical evidence that you will be unable to work for at least a full year, there is no need to wait for the year to elapse before starting!

If you have not been off work for an entire year, but your condition is expected to last at least that long, you should apply right away.

If your condition is not expected to get better, or if a long course of treatment is planned that would take you out past one year, then you can file your initial application. If there is clear medical evidence that you will be unable to work for at least a full year, there is no need to wait for the year to elapse before starting!

If you have not been off work for an entire year, but your condition is expected to last at least that long, you should apply right away. Benefits can’t begin until you have been disabled for five months, and an initial application usually takes 3-5 months (sometimes longer) to process, so the sooner you file your application, the sooner you may get your benefits.

Of course, Social Security may deny your claim initially anyway, in which case you should appeal the decision. We have had several clients who hit the one-year duration mark while we were in the appeals process. A Social Security claim can take up to two years (sometimes longer) from the initial application until adjudication at a hearing, so the sooner you start, the better.

If your diagnosis is terminal, Social Security will make every effort to expedite the processing of your claim. I find it heartening that we don’t receive many inquiries for assistance from people with terminal conditions; I take this to mean that Social Security is doing the right thing and approving them right away.

Social Security has a list of conditions that are automatically approved, called Compassionate Allowances Conditions – if you, or a loved one, are diagnosed with a severe or aggressive condition, you may qualify to be immediately approved! Check the following list at Social Security’s website:

When you file your application, be sure to point out that you believe your condition is on the list.

I also receive calls with a variation on this question, from folks who are still working: “How can I get my Social Security started, so I can stop working?” This call is not from people who are attempting to somehow ‘game’ the system, but rather folks who have been told by their doctors that they should stop working, or people who know that their work activity is exacerbating their medical conditions – but who can’t afford to stop working without a guarantee of income. Unfortunately, this is one of the many Catch 22s of the Social Security Disability world – there is no way to get your benefits started up, until you stop working*.

One of the first things that Social Security will do, when you file your application, is look up your recent and current earnings. If you are still working at a level considered above SGA (Substantial Gainful Activity), then they will not even order your medical records. The fact that you are working, proves that you can – whether or not your doctor has said that you shouldn’t, whether or not you are in pain, whether or not working is causing your condition to get worse.

Please, do not hesitate to contact us if you have questions about Social Security Disability.

*There is a level of earnings under which Social Security doesn’t count your income against you; this level is called “Substantial Gainful Activity”, and it can vary from year to year. In 2013, earnings under $1,040 per month are considered less than Substantial Gainful Activity, though any earnings will cause Social Security to more closely scrutinize your claim (considering, for example, whether you could perform your currently part-time job on a full-time basis, etc.). A year-by-year look at the Substantial Gainful Activity amounts can be found at http://www.ssa.gov/oact/cola/sga.html

The Social Security Administration turns down many worthy applicants when they first apply.

There is a lot in the news these days about the Social Security Disability Program, with some pundits suggesting people are getting on benefits simply because they are unemployed, or because they claim to be injured or ill when in fact they are able-bodied and fully capable of working. Every day, all day, I work with people filing for Social Security Disability benefits. So I work with the program’s rules – yes, there are rules for deciding these cases – it is not enough just to claim to be disabled. And I come face to face with individuals who are struggling, sometimes with a major health issue such as cancer, or rheumatoid arthritis, or Multiple Sclerosis. Other folks have multiple health problems that have combined to force them from the labor market. All of them have medical records, often reams of them, documenting diagnoses, chronicling surgeries and other treatment regimens. This is one big thing I think the general public does not know: a person must have one or more diagnoses from a qualified physician that could account for the symptoms and limitations he or she is reporting to Social Security. There must be convincing medical documentation. Much of my day is spent obtaining and reviewing the medical records of my clients, and ensuring that the decision-makers at Social Security also see them.

…the medical condition must be not only serious, but also prolonged.

Many people are not familiar with Social Security’s definition of disability or the program’s rules, so they do not realize that the disabling medical condition or conditions must be serious enough to have prevented the person from working for AT LEAST 12 continuous months. If the individual has not yet been out of the labor market for a period of at least one year, it must be very clear that this will be the case. In situations where there is doubt about this, Social Security typically turns down the claim. I have had callers who have been unable to work for a few months while going through chemotherapy treatment for cancer, but have been able to get back to work in less than one year. They do not qualify for Social Security Disability benefits. So the medical condition must be not only serious, but also prolonged.

One broadly held belief about Social Security Disability is, in fact, true: The Social Security Administration turns down many worthy applicants when they first apply. It is necessary to appeal (the first appeal is called a Request for Reconsideration). Often, a second denial follows. Then it is necessary to request a hearing in front of a judge. For a person who is too sick to work, not feeling well, and home alone trying to navigate this system, it can be daunting. One of the joys of my practice is our capacity to lend support to such individuals, to take the reins of the case and drive it forward, so my client can concentrate on taking care of herself or himself while I and my staff handle the legal stuff.

We are able to offer representation to people at any stage in the process, including initial application. We are happy to talk with callers who are weighing their options, and simply need information in order to know whether to apply for benefits in the first place. There is no charge for such calls, so do not hesitate to contact us if you have questions about Social Security Disability.

Today’s post comes from guest author Jon Gelman from Jon Gelman, LLC – Attorney at Law.

A settlement was recently reached in a pending Federal Court case tht will benefit Medicare beneficiaries who require skilled services. The Centers for Medicare and Medicaid Services (CMS) will no longer require that a patient “improve” inorder to be entled to services. Jimmo v. Sebelius, No. 11-cv-17 (D.Vt.), filed January 18, 2011

“New policy provisions will state that skilled nursing and therapy services necessary to maintain a person’s condition can be covered by Medicare.”

The Social Security Administration has added to its list of compassionate allowances a pulmonary condition that has been identified as arising out of exposures to burn pits fumes and dusts in Iraq and Afghanistan.

“If a worker becomes eligible for both workers’ compensation and Social Security disability insurance benefits, one or both of the programs will limit benefits to avoid making excessive payments relative to the worker’s past …

An employer cannot stop paying workers’ compensation benefits merely because the injured worker was awarded Social Security Disability benefits. In fact, the premature termination of temporary disability benefits was …

The Social Security Administration has added to its list of compassionate allowances a pulmonary condition that has been identified as arising out of exposures to burn pits fumes and dusts in Iraq and Afghanistan.